European Equities Microstructure

Here's a TLDR note on European equities microstructure.

How are European Equity Markets Structured?

Thanks to the original Mifid which came about in 2007, we have both primary and secondary venues in Europe to (in part) promote competition. These secondary venues are MTFs like CBOE Europe and we've seen significant consolidation in this space since the first Mifid (BATS and Chi-X now being part of CBOE). Europe also has plenty of internalisers, dark pools and OTC venues. Overall a more fragmented market when it comes to liquidity.

Most trading is continuous (outside of the open and close), but venues like Deutsche Boerse also operate periodic intraday auctions.

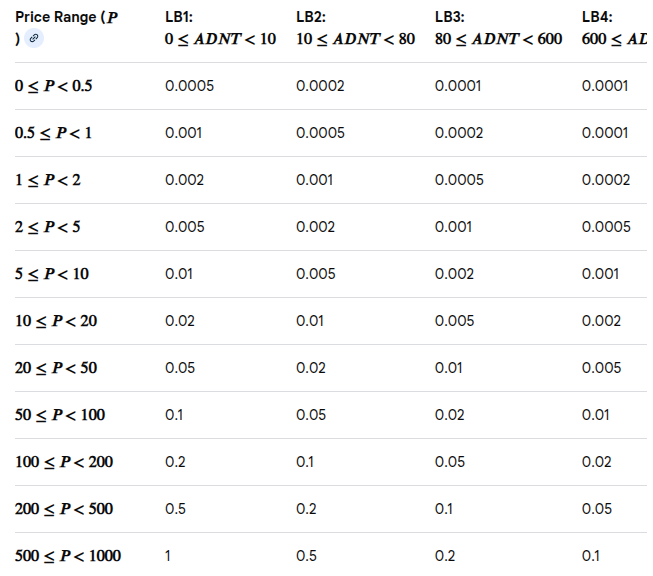

Tick Sizes

Europe uses a harmonised tick size regime to prevent “tick size arbitrage” between venues and to ensure standardize price increments across the EU and UK.

Ticksizes are calculated using the average number of daily trades (which define a stock's liquidity band) as well as other factors like the price (which define the price band of the stock).

Darkpools and SI's can execute at prices which are not multiples of the ticksize i.e. mid point matching.

Here's a sample ticksize table for illustration:

Compared to US Equities

| Europe | U.S. | |

|---|---|---|

| Regulatory framework | MiFID II | Reg NMS |

| Listing venues | Multiple national exchanges | NYSE, NASDAQ |

| Off-exchange trading | MTFs, SIs, dark pools | ATSs, wholesalers |

| Consolidated tape | No | Yes |

| Tick sizes | Harmonized by MiFID II | Fixed by SEC |

| Post-trade reporting | Trade reporting venues (APAs) | FINRA/TRFs |

Venue Locations

Now that Euronext has moved to IT3 in Bergamo (Italy) there are fewer and fewer locations/DCs you need to be in to operate a European Equities franchise. Eurex and Xetra are in Equinix FR2 with CBOE being in Slough (LD4). LSE is now in Telehouse, though tbh I am not entirely au fait these days and optimising fresnal zones on a sub 10m throw is not really my bag now.

-

FLAP = Frankfurt, London, Amsterdam, Paris

-

FLAP-D = FLAP + Dublin

Mifid 1 (2007)

-

Ended the primary exchange monopoly

-

Passporting regime - firms authorised in one EU state could operate across the EU

-

Best execution requirement - must take “all reasonable steps” to achieve best result for clients (best effort best ex)

-

Pre and post-trade transparency

-

Client classification as Retail, Professional, Eligible Counterparty

Mifid 2 (2018)

-

Expanded transparency - beyond equities to bonds, derivatives, ETFs

-

Introduction of OTF (Organised Trading Facility) for non-equities

-

“Double Volume Cap” limits dark pool trading (4% per venue, 8% total per stock)

-

Stricter quoting and reporting obligations for internalisers

-

Research unbundling - no soft comms, clients must pay separately for research and execution

-

Algorithmic & HFT regulation - Mandatory controls, testing, and market-making obligations

-

Tick size harmonisation (RTS 11) - Pan-EU dynamic tick size regime based on liquidity bands and price bands

-

More granular reporting